Featured

Table of Contents

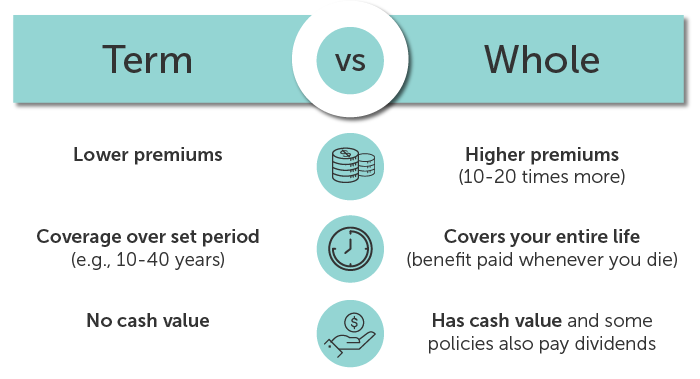

Several entire, universal and variable life insurance coverage policies have a cash worth component. With among those plans, the insurance provider transfers a section of your monthly costs settlements right into a money worth account. This account earns rate of interest or is invested, assisting it expand and provide a more considerable payout for your beneficiaries.

With a degree term life insurance policy, this is not the instance as there is no cash money worth part. Because of this, your plan won't expand, and your fatality advantage will certainly never ever boost, therefore limiting the payout your beneficiaries will obtain. If you want a policy that gives a survivor benefit and develops cash money value, look into whole, universal or variable strategies.

The second your plan runs out, you'll no longer live insurance policy protection. It's often possible to renew your policy, but you'll likely see your premiums raise significantly. This could present concerns for retired people on a fixed earnings because it's an added cost they could not be able to manage. Degree term and decreasing life insurance offer similar plans, with the major difference being the survivor benefit.

(EST).2. On the internet applications for the are available on the on the AMBA internet site; click the "Apply Now" blue box on the right-hand man side of the web page. NYSUT members can additionally publish out an application if they would like by clicking the on the AMBA website; you will then need to click on "Application Kind" under "Forms" on the right-hand man side of the page.

Level Term Life Insurance Vs Whole Life

NYSUT participants enrolled in our Level Term Life Insurance Policy Strategy have actually access to provided at no extra price. The NYSUT Member Benefits Trust-endorsed Level Term Life Insurance Policy Strategy is financed by Metropolitan Life insurance policy Company and administered by Organization Member Perks Advisors. NYSUT Student Members are not eligible to take part in this program.

Term life insurance is a budget-friendly and uncomplicated option for many individuals. You pay premiums each month and the insurance coverage lasts for the term length, which can be 10, 15, 20, 25 or thirty years. But what happens to your premium as you age depends on the kind of term life insurance policy protection you get.

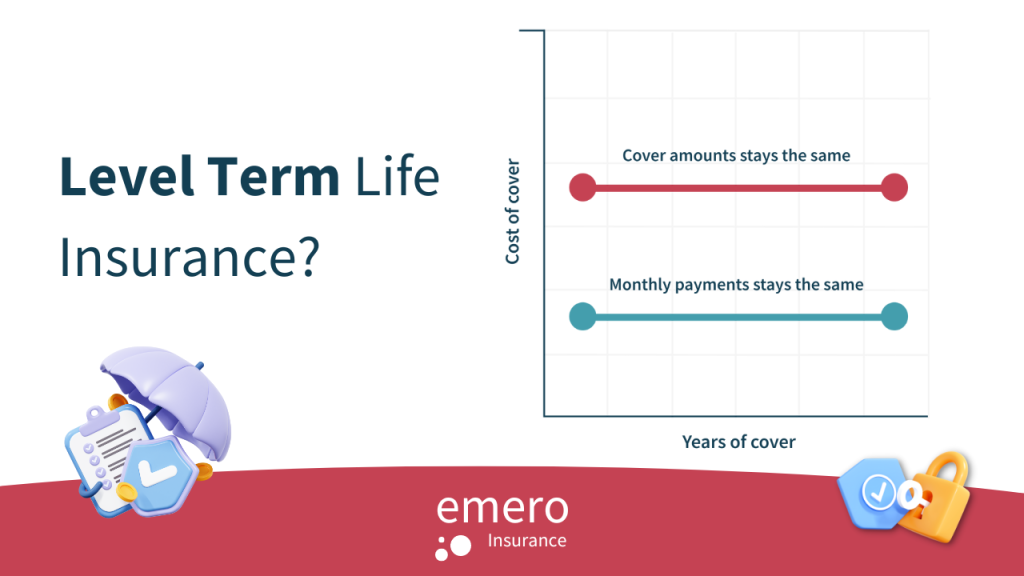

As long as you remain to pay your insurance coverage premiums each month, you'll pay the exact same price throughout the entire term size which, for lots of term policies, is usually 10, 15, 20, 25 or thirty years (Level term life insurance protection). When the term ends, you can either select to end your life insurance policy coverage or renew your life insurance policy plan, normally at a higher price

What should I know before getting Tax Benefits Of Level Term Life Insurance?

For instance, a 35-year-old female in excellent wellness can acquire a 30-year, $500,000 Place Term plan, provided by MassMutual starting at $29.15 per month. Over the next 30 years, while the policy remains in area, the expense of the insurance coverage will not change over the term duration. Let's face it, a lot of us don't such as for our bills to expand over time.

Your degree term rate is identified by a number of variables, a lot of which belong to your age and health and wellness. Various other factors include your details term policy, insurance company, benefit amount or payout. Throughout the life insurance policy application procedure, you'll respond to questions regarding your wellness history, including any type of pre-existing problems like a crucial disease.

Bear in mind that it's always really vital to be straightforward in the application process. Issuing the plan and paying its benefits depends on the applicant's proof of insurability which is figured out by your solutions to the health and wellness inquiries in the application. A medically underwritten term plan can secure an inexpensive price for your insurance coverage period, whether that be 10, 15, 20, 25 or 30 years, no matter exactly how your wellness could alter during that time.

With this sort of degree term insurance coverage, you pay the exact same regular monthly costs, and your beneficiary or beneficiaries would get the exact same benefit in case of your fatality, for the entire insurance coverage duration of the plan. So just how does life insurance work in regards to expense? The expense of level term life insurance will certainly depend upon your age and wellness along with the term length and insurance coverage quantity you select.

What does No Medical Exam Level Term Life Insurance cover?

Life: AgeGenderFace AmountTerm LengthPremium30Male$500,00030$29.9930 Female$1,000,00030$43.3135 Male$500,00020$20.7235 Female$750,00020$23.1340 Male$600,00015$22.8440 Women$800,00015$27.72 Quote based on pricing for eligible Sanctuary Simple applicants in outstanding wellness. Rates distinctions will differ based upon ages, health status, protection quantity and term length. Sanctuary Simple is presently not offered in DE, ND, NY, and SD.Regardless of what coverage you select, what the plan's cash money value is, or what the swelling sum of the death advantage ends up being, comfort is amongst one of the most valuable benefits related to buying a life insurance policy plan.

Why would certainly a person select a policy with an each year sustainable costs? It may be an option to take into consideration for somebody who requires coverage only momentarily. As an example, a person who is between jobs yet desires survivor benefit defense in place since he or she has financial debt or various other economic responsibilities might wish to consider an every year renewable policy or something to hold them over till they begin a brand-new job that provides life insurance policy - Compare level term life insurance.

You can normally renew the policy annually which offers you time to consider your alternatives if you want insurance coverage for longer. Realize that those choices will certainly entail paying greater than you utilized to. As you age, life insurance policy costs become significantly much more expensive. That's why it's useful to purchase the correct amount and size of insurance coverage when you initially obtain life insurance policy, so you can have a low price while you're young and healthy.

If you add important unpaid labor to the house, such as childcare, ask on your own what it might set you back to cover that caretaking job if you were no more there. Make sure you have that coverage in location so that your household gets the life insurance benefit that they require.

What is the difference between Level Term Life Insurance Premiums and other options?

For that set quantity of time, as long as you pay your costs, your rate is secure and your beneficiaries are shielded. Does that indicate you should always choose a 30-year term length? Not always. Generally, a much shorter term plan has a reduced costs price than a longer plan, so it's smart to choose a term based upon the projected size of your financial duties.

These are very important aspects to bear in mind if you were believing regarding selecting an irreversible life insurance policy such as a whole life insurance plan. Several life insurance coverage plans give you the alternative to add life insurance riders, assume added benefits, to your plan. Some life insurance policy plans feature riders integrated to the expense of premium, or cyclists might be readily available at a cost, or have fees when exercised.

With term life insurance, the interaction that the majority of people have with their life insurance policy business is a month-to-month costs for 10 to 30 years. You pay your regular monthly premiums and wish your family members will never ever have to utilize it. For the group at Sanctuary Life, that appeared like a missed out on chance.

{kind=link}

Table of Contents

Latest Posts

Funeral Protection Insurance

Metlife Burial Insurance

Final Expense Protection

More

Latest Posts

Funeral Protection Insurance

Metlife Burial Insurance

Final Expense Protection